Best UK Islamic Bank Savings Rates Today (July 2026)

Adil Hussain

24 July 2026 2 min read

Mohsin Patel

Co-founder

4 min read

Last updated on:

A Lifetime ISA is an account which lets you save up to £4,000 a year with the government adding a 25% bonus. So if you save the maximum, that’s a tidy £1,000 in your pocket. In the investment world, a 25% return is pretty astounding.

I’m not going to go in-depth on the actual product here. There are lots of good mainstream places (such as MSE) that you can search for and look at.

The focus in this article is for Muslims who are hesitating on whether a LISA is halal. We’re going to reveal when the LISA is halal and when it isn’t. We’re also going to reveal a hack that you’ll find very helpful.

That’s right – the LISA itself can be both haram or halal, depending on where you open one and what you put in it.

Don’t let that put you off though: it’s easy once you know what to look out for. Just follow our guide and you’ll be saving in your LISA in no time.

Let’s kick off with a key question.

The key benefit of a LISA is the 25% government bonus. You must be wondering whether this is riba or haram for some other reason.

The good news is that a government bonus is perfectly permissible. We’ve explained the logic on this before when we discussed Help To Buy ISAs and the Help To Save scheme.

Basically, this isn’t like a standard commercial transaction where you get a return for your money. It’s a governmental scheme for very specific purposes (you can only withdraw the money penalty-free if you’re buying a home or retiring).

From a fiqhi perspective, it is seen as a gift.

In short, we’re fine on this front.

The government bonus isn’t the tricky part. The tricky part is then understanding where to open a LISA.

The reason for that is because like a normal ISA, there are basically two types:

These are unequivocally haram because they invariably pay interest on your cash. To be clear, we’re not talking about the 25% government bonus here. We’ve already said that’s fine.

What we’re talking about here is the bog standard cash LISA offered by the main banks and building societies. For example this one by Skipton Building Society.

If there happened to be a cash LISA that paid no interest, that would be fine.

I doubt you’ll find one though as the mainstream market will always want an interest return for depositing cash.

Check out my hack below though for how to find a no-interest LISA account.

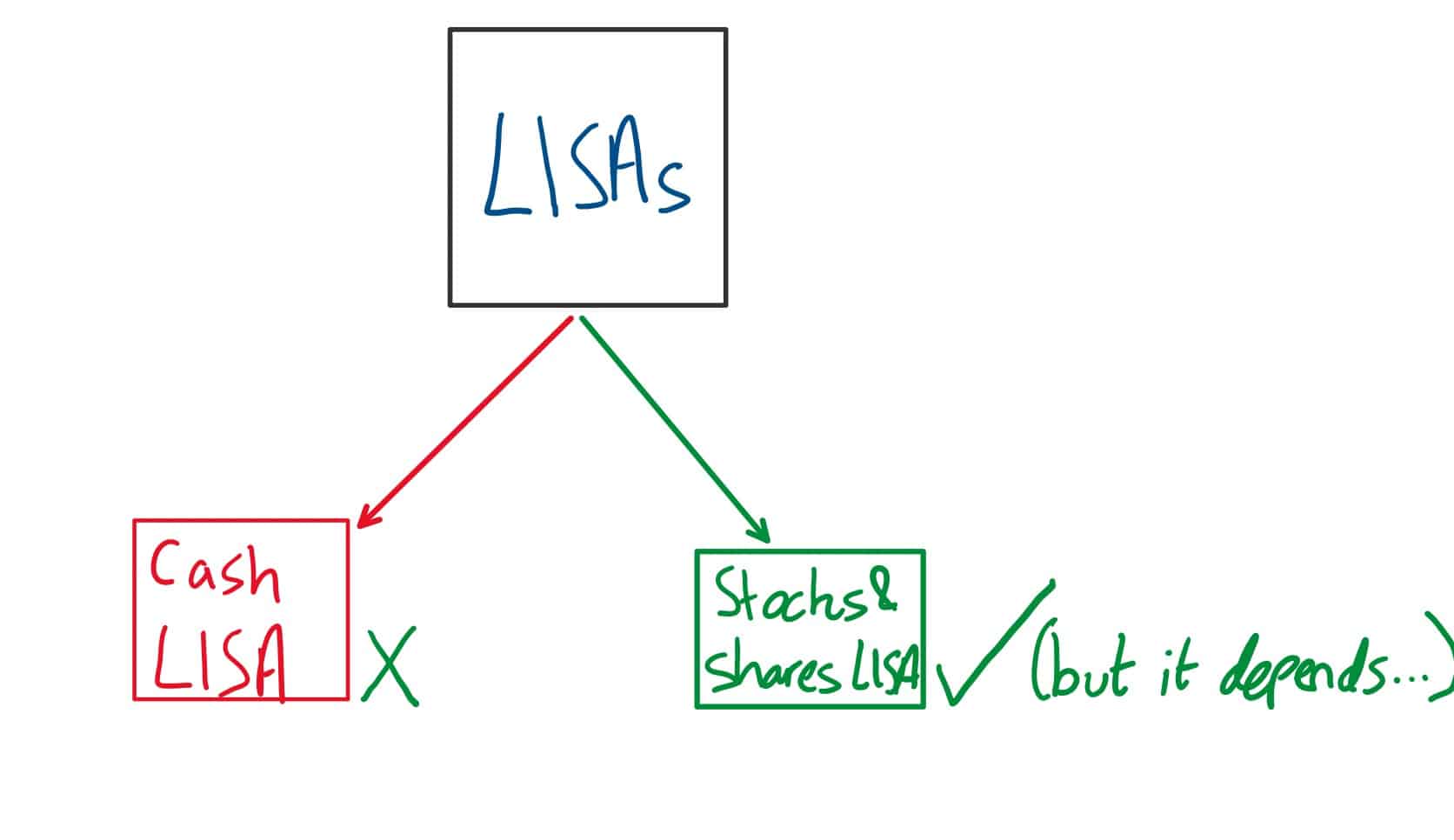

We’ve ruled out cash LISAs and we’re left with stocks & shares LISAs. These must be halal right? Well, it depends.

You see a stocks and shares LISA is a bit like opening a Just Eat account. But swap eating for investing.

In your Just Eat account, you can choose from lots of halal places, but there are also a lot of haram takeaways too. It’s the same with a stocks and shares LISA: you can choose from lots of halal companies to invest in, but there are loads of haram ones too.

The key point is this: so long as your stocks and shares LISA has halal investments within it, it’s halal for you. Same ruling for Just Eat by the way.

Here’s a (very) fancy graphic I drew to summarise.

I hear you but I am still going to try and convince you that investing isn’t scary and you don’t need to be Warren Buffett.

Here’s why you shouldn’t be scared: if you go for an AJ Bell LISA or a Hargreaves Lansdown LISA, you’ll be able to select from a bunch of sharia-compliant funds.

If you don’t know what a fund is, it’s basically a basket of companies that have been pre-chosen by a specialist fund manager.

You’ll have to pay a small management fee to buy into the fund, but in return you’re getting the opportunity to benefit from the value of the fund increasing because the shares have hopefully done well.

By buying a fund, you’re also not having to worry about choosing which shares to buy yourself.

So you could deposit your £4,000, get your £1,000 bonus for year 1, and invest the lot in a sharia-compliant fund. If that fund price increases by say 8%, you’ll be up a further £400.

Obviously fund prices can go up and down so you are exposing yourself to loss too, but over time, the stock market tends to smooth out.

I’ve mentioned AJ Bell and Hargreaves Lansdown as I know they have decent Islamic options in their fund offerings. You can take a look at them in our halal investing comparison page.

Not every Islamic home purchasing plan will allow the use of LISAs. Currently only Strideup and Gatehouse Bank's HPP will allow the use of LISAs. For shared ownership options such as Pfida and Wayhome, you won't be able to use a LISA so keep that in mind when choosing whether to open a LISA or which home purchasing provider to go with.

LISAs are perfectly halal as long as you go for a stocks and shares LISA and you’re investing in halal stuff (or keeping it as cash only and attracting zero interest, e.g. with an AJ Bell stocks and shares LISA). Head over to our halal investment comparison page to see which sharia-compliant funds you can invest in and on what platform.

If you want to learn more about the other forms of ISAs, check out this complete guide.

Mohsin Patel

Co-founder

Mohsin is the co-founder of IslamicFinanceGuru, an Oxford graduate and a Forbes 30 under 30 alumnus. He's a former corporate lawyer at one of the world's largest US firms. Whilst running IFG, Mohsin is also actively interested and invested in the web3/crypto space. Publication: Halal Investing for Beginners: How to Start, Grow and Scale Your Halal Investment Portfolio (Wiley) Mohsin is the co-founder of IslamicFinanceGuru, an Oxford graduate and a Forbes 30 under 30 alumnus. He's a former corporate lawyer at one of the world's largest US firms. Whilst running IFG, Mohsin is also actively interested and invested in…

24 July 2026 2 min read

15 July 2026 6 min read

14 July 2026 8 min read

Leave a Reply