Best UK Islamic Bank Savings Rates Today (July 2026)

Adil Hussain

24 July 2026 2 min read

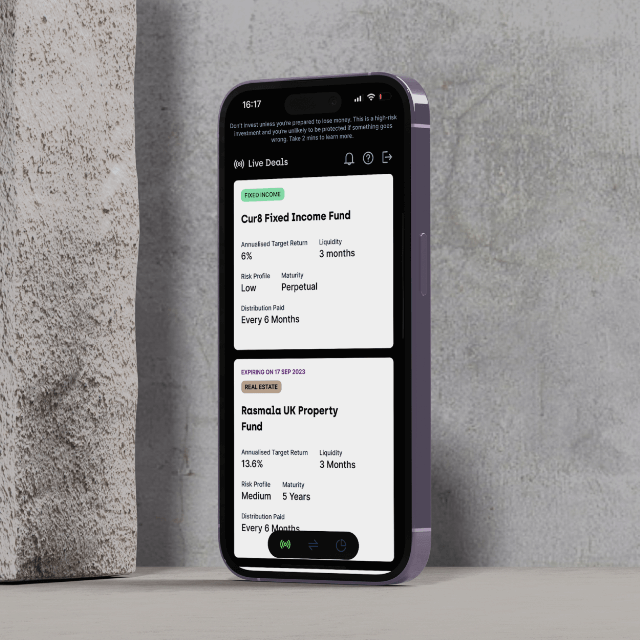

Here are the wide array of Islamic financing options available

There are now a number of halal home financing providers in the UK. You can check them out on our compare page.

Islamic Mortgage Comparison

Estimated Islamic mortgages issued annually

Average mortgage debt in the UK

Islamic home finance providers in the UK

Unfortunately, things are still a little patchy when it comes to business finance.

In the UK, for SME businesses you should check out Qardus. Asset financing is often halal too (so check out people like Investec for this).

Overseas, there are now a range of options in the Middle East such as Funding Souq, Erad, Lendo and many others.

For startup funding, we can potentially help at cur8.capital (we only focus on high potential tech startups though and we unfortunately have to be pretty picky).

There are now other players like Maydan Capital, Ethis in Malaysia and Falcon Network in the UAE. You should check them out too.

Master the AAOIFI Standards with Usul Fiqh and Maqasid Shariah: A Comprehensive Two-Year Study Program

Enroll in Course Explore DetailsFor savings accounts and current accounts there a number of banks to choose from

Traditional banks include: Al Rayan, Gatehouse, Al Ahli, BLME, QIB (UK) and Habib Bank AG Zurich. Digital (neobanks) include: Kestrl, Nomo, Algbra and Niyyah.

We did a detailed comparison between them.

View Comparison

Riba is commonly translated to ‘interest’ or ‘usury’ in English and is a charge for the use of another’s money. It also includes unequal exchanges.

An example of this would be taking a loan from someone who expects it to be repaid in addition to 5% per month on anything that has not been paid at the end of each month.

So, for example, you lend £100 for one month. At the end of that, you would repay £105.

Riba plays an important part in Islamic Finance because interest is forbidden and Islamic Finance looks to create Financing options for Muslims that are shariah-compliant and without riba.

You can read about Riba in depth here.

Gharar means ‘uncertainty’ and is associated with deception involving uncertainty and risk. It is rooted in the Arabic word ‘to deceive’ (gharra).

Gharar is a broad concept and can involve:

Gharar can include:

You can read more about Gharar here.

In order for an investment to be halal, it must be compliant with the regulations and principles set out by Islam in the Quran and sunnah (known as ‘shariah law’).

There is nothing inherently haram (impermissible) about earning money through profit distributions from business activity or from the increase in value of assets.Read about the halal investment criteria here.

For a property investment to be halal, each investment and element of the investment contract must be in line with shariah.

This requires that:

Read about this in detail here.

Riba (interest) is prohibited in Islam because it is seen as exploitative, treats money as a commodity rather than a medium of exchange, and undermines economic justice. Learn more about why riba (interest) is haram in Islam in our full guide.

24 July 2026 2 min read

24 July 2025 15 min read