Our Community Needs to Start Financing Its Own Future

Zain Karbani

15 July 2026 6 min read

Haider Saleem

9 min read

Last updated on:

There are two great ways to invest your money – in property or though crowdfunding. But only if there was a way to do both? Luckily for you, CrowdToLive* has done just that, by combining these and providing investors with a way to diversify their portfolio in bricks and mortar.

CrowdToLive is a low-cost sharia-compliant property crowdfunding platform that connects investors to those wanting to get on the property ladder. If you are looking to get onto the property ladder then check out their offering to you here.

In this article, we’ll discuss:

We’re briefly going to go over some basics before we dive into our analysis – just so we’re all on the same page.

Crowdfunding is a public way of raising money from many people for a specific goal. This is mainly done online and especially through crowdfunding websites. Once all the money is pooled together, the capital is used to finance the project or goal.

CrowdToLive does exactly this when they are raising funds to purchase a property (more on that later).

We have a detailed article on crowdfunding here, including a list of platforms on which you can invest.

Many people can’t afford to buy a home on the open market. It’s an expensive commitment.

CrowdToLive is one of the alternative solutions, which uses a shared ownership model when it purchases a property. However, it’s slightly different from the traditional model discussed below – we’ll explain it in more detail. CrowdToLive purchase the property under the Musharakah structure.

A shared ownership scheme means you buy a share of a property and pay rent to an organisation for the remaining share. For/not-for-profit organisations and the government offer these type of ownership schemes.

This is a great option for those on a low income, little capital or no help from The Bank of Mum and Dad.

Shared ownership is one of the many alternatives to a mortgage that you can read about here. It is also unambiguously and unanimously seen as a halal way to buy a property (and to invest).

Now we all understand the basics, let’s dive in.

CrowdToLive is a property crowdfunding platform that connects a Champion (the person that wants to raise equity financing) to a pool of investors, enabling them to join together and purchase a property.

You can either chose to be a Champion if you’re seeing to raise finance or be an investor to seek profitable returns.

Champions will reach out to CrowdToLive, who will advertise projects to potential investors. Once the investment fulfils its goals, CrowdToLive then provides:

In this article, we’ll focus more on the investing side, which is explained next.

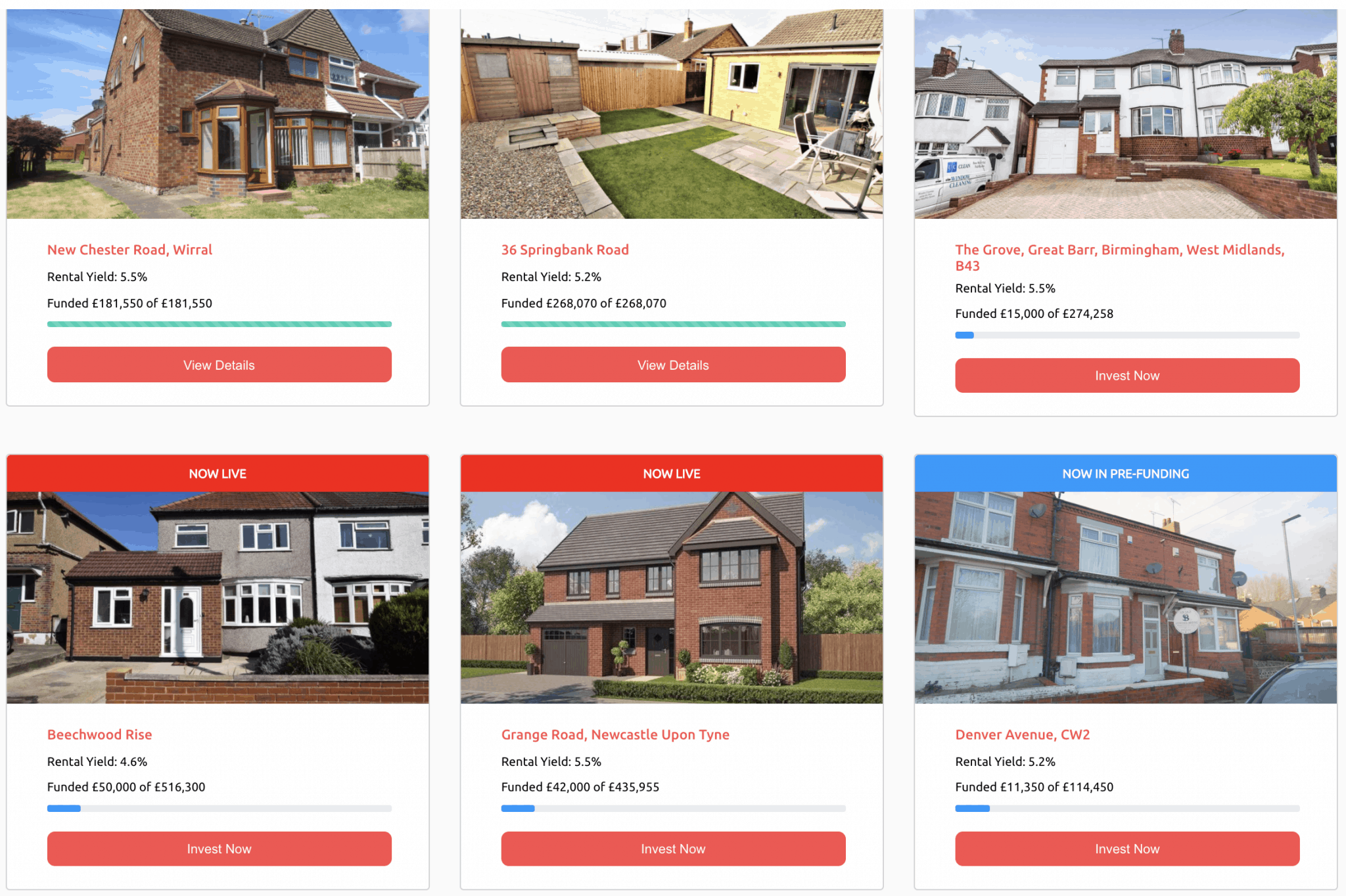

They offer high net worth and sophisticated investors a long-term investment opportunity in purchasing a property through a sharia shared ownership scheme. The minimum investment is only £100. They provide a range of properties to invest in, some of which you can see below.

As you’ll see, there’s a range of properties and yields. The properties also have a short bio of the tenant, so you know exactly who’ll be living there.

The yields are what you’d expect o average on a BTL. Although if you do it yourself, you can find higher yields of 10% or more. You can find these areas in our article – The Best Places to Buy A Buy-To-Let In 2021. (caveat: It’s not easy to do yourself.)

On CrowdToLive on the other hand it is very much hands-off. You can buy properties and manage your money through their analytics dashboard, making it easy to track your money.

You buy unlisted shares in a company. This is how it works:

There are two ways your investment can get a return:

As we mentioned, the company must raise money and invest in a property with a Champion. The minimum investment starts at £5,000.

This money raised will be used to buy a property. The property will be rented out to the Champion will be pay rent. Any profit from the rent (i.e., after company expenses and taxes) will be distributed as a dividend by the company.

Rent will increase yearly at each annual anniversary of the lease by the rate of inflation.

Furthermore, you could potentially benefit from the capital appreciation of the property. Therefore, you could sell your shares at a higher price than you bought them for. However, it may not be easy to sell your shares as they are unlisted. Therefore, you’ll have to find a buyer yourself.

You can reduce your investment risk by diversifying in several properties in different locations. This has the additional benefit of diversifying your portfolio.

A platform fee is payable and there is 3% payable upfront.

This will be charged to investors on a successful investment.

However, if you invest in a property that does not complete for whatever reason, no fees will be charged.

The maturity of the initial investment is 5 years but can be renewed with the consent of the majority investor. As long as the Champion is paying the rent, the property cannot be sold. However, you can sell your shares whenever you like, if you can find a buyer.

The Champion has the option, but not the obligation, to buy investors shares to increase his homeownership.

You’ll of course be responsible for your own taxes. Each company you invest in will be liable to pay corporation tax and any returns you receive will be paid to you net of any corporation tax due.

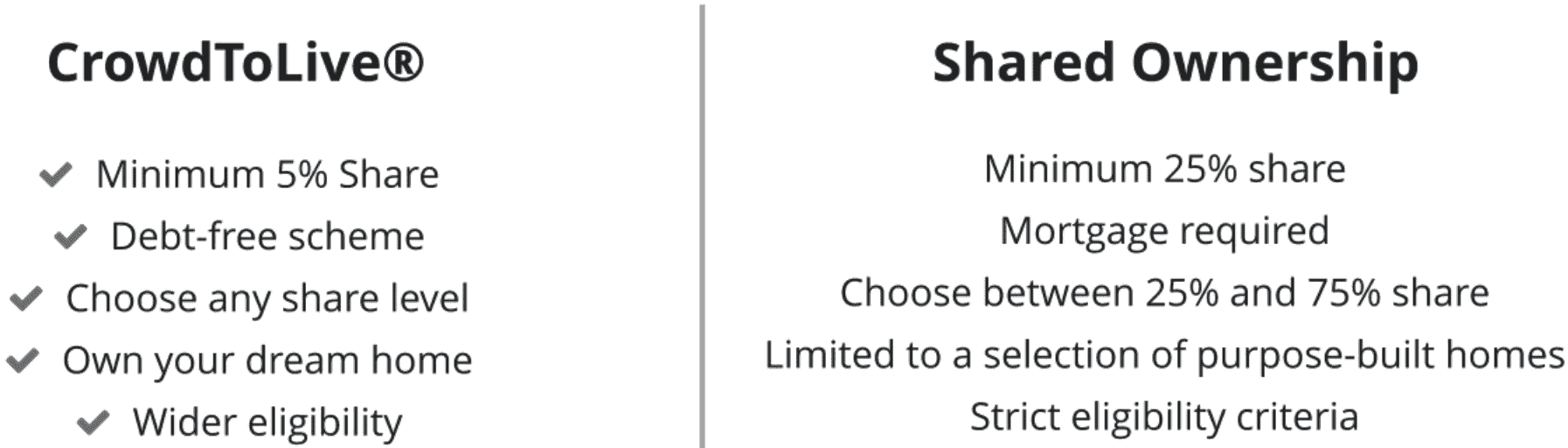

CrowdToLive purchases the property under the Musharakah structure and there are some notable differences from the traditional shared ownership model. They have handily summarised this in the graphic below:

CrowdToLive v traditional shared ownership. Source: CrowdToLive.

A key difference is that a shared ownership scheme has a limited chose of properties to purchase. In contrast, CrowdToLive allows you to choose any house on the market.

The minimum share is a big one too – the Champion only needs to invest 5% of the purchase price rather than 25%.

CrowdToLive believe they offer an efficient alternative to Buy to Let. They argue this for three reasons:

However, the advantages of a BTL are:

CrowdToLive is operated & owned by Elite Capital and Management Services Limited. The founding team have a long background in Islamic banking both in the UK and abroad, and they are an FCA-regulated company.

Let’s have a look at the good and bad.

You can invest through their website here.

Housing is a massive issue here in the UK. I’ve highlighted a few below that makes me think CrowdToLive have a promising future:

What I like about CrowdToLive is that it really does help to answer some of the big issues. It obviously won’t find a solution to the building problem and lack of supply, but the fact that you can get on the property ladder with just a 5% deposit really does open doors for many people.

You could argue that their offering is better than the government’s Help to Buy scheme, as that is only available to purchase new builds and requires you to take out a mortgage. This clearly won’t be practical for some who want a different type of property and do not want a mortgage.

The UK market currently hosts more than 40 property crowdfunding platforms, out of which 10 have been founded within the past three years. Clearly, this is a growing area and competition will increase.

Ultimately though, CrowdToLive will need to find deep institutional lines of capital in order to significantly scale their business. That’s just the way it is with property. We hope they succeed in this endeavour inshAllah.

It is key that an investor has some fixed return products to diversify their portfolio. CrowdToLive is certainly one to consider.

The platform is designed for anyone that wants the benefits of being a landlord without all the work. It requires only £100 to get started and you’re making money whilst helping someone who can’t afford a home get on the property ladder. Most importantly, not only is it ethical, but it’s also completely Islamic.

For other fixed income investing ideas – check our full Halal Fixed Income Investing 101 Guide.

If you enjoyed this article, you can follow me on Twitter or LinkedIn.

Haider Saleem

Haider is a BBC-trained journalist, trainee solicitor and member of the IFG content team. Haider is a BBC-trained journalist, trainee solicitor and member of the IFG content team.

15 July 2026 6 min read

14 July 2026 8 min read

Leave a Reply