Our Community Needs to Start Financing Its Own Future

Zain Karbani

15 July 2026 6 min read

IW

IFG Staff Writers

11 min read

Last updated on:

by Mohammed Ayaaz Adam

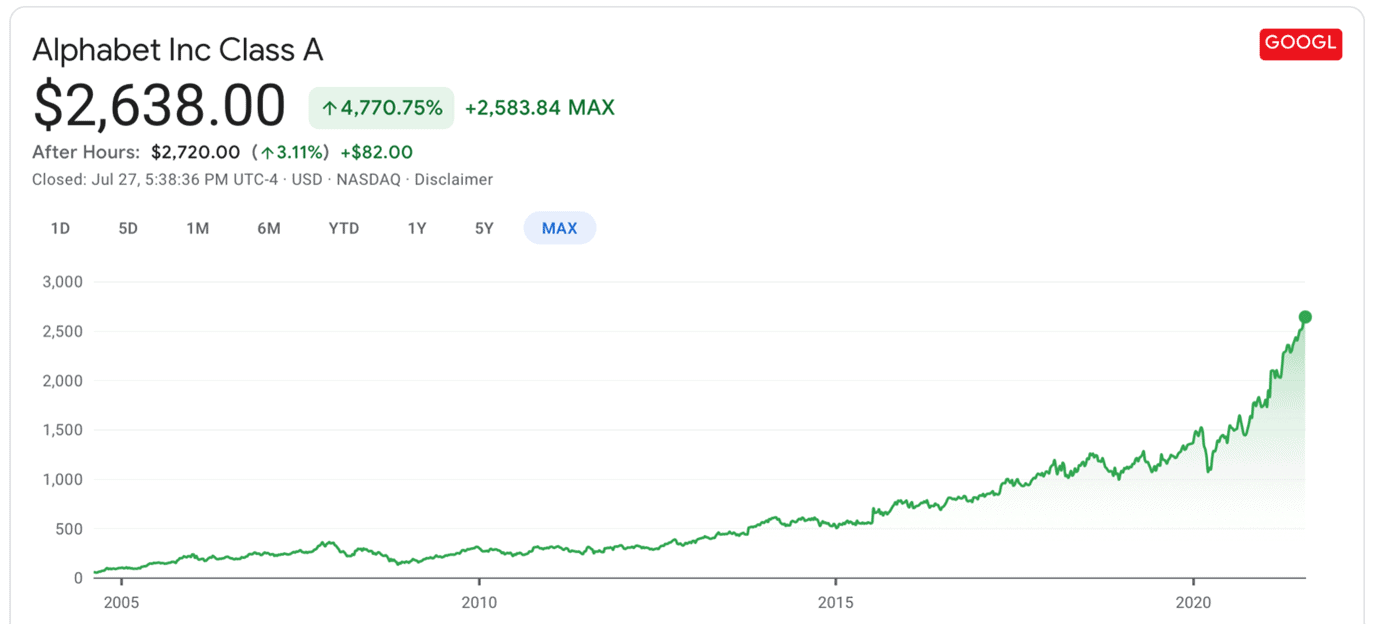

If you could go back in time to 2004, would you rather have invested in the IPO of tech behemoth Google or the pizza franchise Domino’s?

Tech stocks have seen some of the highest growth in the past few decades, so most people would say Google in a heartbeat.

Surprisingly, until a few months ago, you would have been better off investing in Domino’s.

This is a story about how Domino’s outperformed one of the most significant businesses in the modern world. And why nearly everyone overlooked Domino’s.

N.B. this is not a comment on the sharia-compliance of Domino’s. For sharia-compliant stock investing ideas you should check out IFG Fund Replicator.

The common themes across technology companies are an oft-repeated cycle of innovation, disruption, and mass adoption.

This potential for societal disruption and mass adoption means more investment flows into the tech sector, and high levels of sales are made since there is a clear blue ocean with a lack of competitors and so everyone can be a potential customer.

Think about Google. When it first began in 1998, its user base was low but its potential user base was virtually unlimited. This potential is what gives tech companies higher valuations and higher growth.

Growth stocks are growth stocks because people believe they will grow into their higher valuations because of high sales growth in the future.

Fast forward a couple of decades and billions of people use Google every day, earning them billions a year in ad revenue and driving up their value as a company.

For a software company, the cost of scaling and rolling out their product is inexpensive compared to a physical product. Once you’ve made a piece of software, countless people can buy it. But a pizza franchise has to create a pizza from scratch for each customer.

This difference in distribution and scalability is a huge reason why tech can grow so fast.

But it doesn’t end there. Tech giants like Google, Apple, and Microsoft, are the kings of the tech sector because they are constantly spending their cash to innovate and keep their customers satisfied with the latest tech. By buying shares in these tech companies you are trusting their R&D investment prowess, which is the fundamental reason tech stocks are growth stocks.

This is in stark contrast to a highly saturated space like the restaurant industry.

Anyone living in a city can probably find countless takeaways and restaurants if they just walked around for a couple of miles.

Restaurants compete in a red ocean where each business is a shark looking for blood. It is a cut-throat industry. It comes as no surprise that restaurants have a higher failure rate compared to the economy as a whole.

Domino’s is competing not only with other pizza stores, but with other types of cuisine and restaurants, and also with home-cooking, and now with other delivery services!

Add to that the fact that the restaurant business model has been tried and tested for over two centuries, and you realise that there is not much room for innovation in the sector compared to tech companies where everything is about constant innovation.

This is why it makes sense to intuitively choose Google over Domino’s. It’s simply a matter of understanding the fundamental business model of a tech company vs a food franchise.

It takes a keen investing insight to be able to pick out Domino’s, located in a sector and industry that isn’t high-growth, and hold it for over a decade to realise monumental outlier returns.

Whereas you could have picked a number of good tech stocks and achieved those ‘tech returns’.

We can compare the tech sector and the restaurant industry using representative indices.

Let’s take ‘The Technology Select Sector SPDR Fund’, which is one of the most popular ETFs representing the American technology sector, with the ticker XLK.

This ETF has holdings such as Apple, Microsoft, and Nvidia.

While there are many indices and ETFs that track the technology market, there are hardly any trackers specific to the restaurant and food market. A lot of people want to invest in the former specifically and not the latter!

To represent the restaurant industry we can use the Dow Jones US Restaurants & Bars Index (DJUSRU) or the EATZ ETF (which is the only real ETF specifically in the restaurant space).

Just in the past 5 years, the technology sector (XLK) has returned 237.16% compared to 108.48% for the DJUSRU and 75.17% for the EATZ ETF.

This proves two things: firstly, the tech sector is a higher growth sector. Secondly, it doesn’t take an immense amount of investing prowess to succeed in tech investing since the famous names all seem to have done well in the past few years.

If you invested in any one of the top three holdings of XLK you would have made the following returns in the past five years:

Compared to the top three holdings of EATZ:

How does Domino’s and Google compare against its own competitors?

Finally, let’s compare Google and Domino’s to their own direct competitors to help us understand just how much the success is company-specific, rather than sector-specific.

We’ll use Facebook as a competitor for Google, and Papa John’s as a competitor for Domino’s.

Looking back 5 years, the total returns are:

What we see here is the tech companies performed similarly. But Domino’s massively outperformed its competitor. It’s a clear outlier.

Let’s explore what has allowed Domino’s to achieve these colossal returns.

Domino’s was founded in 1960 in Michigan in the USA.

If you invested at its IPO in 2004, you would have earned a total return of 3790.17%. Until last October, it had a higher performance than even Google.

What has given Domino’s these tech-stock like growth returns?

There are four major factors that makes Domino’s so different and successful compared to its direct competitors and the restaurant industry at large:

Let’s take a look at each one in turn.

Domino’s has end-to-end control of all its franchises.

They work on a model of ingredient centres in their pizza network across a country. One centre produces thousands of dough balls everyday, not to mention countless amounts of ingredients from pre-sliced mushrooms and peppers to the basic cheese and tomato sauce.

These centres then deliver to the thousands of franchises across the country, creating a robust pizza supply network.

This level of supply chain mastery has allowed Domino’s to sustain a high level of quality control across thousands of stores.

Their mass production system for ingredients also allows Domino’s to keep their costs low with a consistently increasing gross margin over the years. In June 2010 their gross margin was 27.69%. They now boast a gross margin of 39.49% as of June 2021.

We can see why investors would prefer this when compared to a direct competitor like Papa John’s, which is not a bad company itself, where its gross margin jumped from 21.97% in June 2010, to 52.33% in September 2010, and has dropped since then down to a 32.35% gross margin, being consistently beaten by Domino’s year after year.

These lower costs also allow Domino’s to compete on price in an industry where every penny counts and profit is hard to come by.

In a world where third party delivery services such as Deliveroo, JustEat, and DoorDash thrive, Domino’s can even outwit them by being able to open in low-density population areas such as suburbs.

Delivery services can’t service rural and suburban areas due to the cost of sending a single order out many miles. Whereas the Domino’s supply chain network makes even these remote locations profitable.

Add to this their in-house delivery drivers and they run circles around their competition.

Domino’s was a delivery-oriented pizza franchise from its inception when it used a Volkswagen Beetle in 1960 to make deliveries in a small town in Michigan.

Fast forward over half a century and they are the uncontested champions in pizza delivery.

Pizza as a food presents a certain ease in the restaurant business. There is a set process for every pizza: dough, cheese and sauce, toppings, pop it in the oven, and you have your product for sale. There are no complicated recipes and processes, no complex mixtures.

This allowed Domino’s to really become highly efficient in delivery compared to other food franchises, whether they be Chinese or Indian food.

This then left other pizza places as delivery competition. With their extensive supply chain and low cost as a result, Domino’s could afford to outdo other pizza deliveries by being able to turn a profit on each delivery in an industry where even breaking even is considered a good result.

But Domino’s hasn’t stopped there. They have consistently innovated as best they can over the years. In 2019, they introduced a delivery insurance where you’re guaranteed a free pizza if anything happens to your delivery.

This level of innovation stretches back in time. They gained a head start by focussing on delivery from their inception in 1960, whereas Pizza Hut was a brand that put all its efforts into the dine-in model.

Even in the early 2000s when Pizza Hut was still succeeding in their dine-in model, Domino’s surpassed them in their outlook on the future by introducing 30 minute deliveries, possible due to their mastery of the supply chain, network, and in-house delivery.

This level of efficiency and profit-making prowess is only possible due to the unique obsession Domino’s has with technology and data, especially for a pizza franchise.

As recently as June 2021, Domino’s completely revamped their mobile apps. With less fewer taps to place an order, and new deals, to being able to invite other people to make a pizza order together, Domino’s is unique in its space by never stagnating in its technology.

It’s very uncommon to see a food franchise put so much emphasis on proprietary software and cutting-edge technology.

Every Domino’s franchise is connected to the Domino’s software. Somewhat infamously, Domino’s forced all its franchises to use its own point of sale system. This means from a customer’s order to every pound and penny made to every ingredient supplied, it is all recorded and inputted into their data models.

Being this data-centric has paid off.

Domino’s has calculated the average time it takes to make a pizza in its store, which allows them to give accurate delivery estimates.

By not being dependent on a third-party software vendor, they have complete control and flexibility when it comes to bugs, tests, and adding new features. This has paid off in the long run by being able to growth hack their way to more sales.

An example of their growth outlook using their data-centric model is seeing that one-third of their customers aren’t too fond of deliveries. To appeal to this segment of their market, Domino’s has enacted a plan to bolster the carry out facilities in their franchises. Talk about data-driven growth.

All this efficiency in tech fundamentally translates to better margins. By taking a gamble in the early 2000s on putting all their resources behind the digital experience, they prepared themselves for the smartphone world that we now live in.

They don’t just sit on all this innovation though, they tell everyone they can with their genius marketing campaigns.

Domino’s IPO’d in 2004, during the same period as Google did.

Having earned a total return of 3,790.17% since then, it didn’t get off to a spectacular start as is evident in the above chart.

Having earned a total return of 3,790.17% since then, it didn’t get off to a spectacular start as is evident in the above chart.

People did not like the taste of their pizza, and no matter how savvy your app is, as a food business if you have not nailed down the food, you have nothing.

Realising this, Domino’s risked their own reputation with a genius marketing campaign.

A year after the 2008 financial crisis, they completely overhauled their recipe and brand with a marketing campaign that disparaged their own recipe. Admitting this, they then advocated for their new recipe.

What was the result of that campaign? Take a look at their chart above and see the growth that took place post-2010. The gamble paid off, and soon they transformed into one of the most profitable stocks in the sector.

Around the time of their IPO, Domino’s wasn’t faring too well in the USA but had decent sales internationally. After their marketing campaign, they gained an unshakeable foothold domestically, and have continued to expand internationally.

Their marketing continues, with most of us having seen a Domino’s leaflet through our letterboxes and countless vouchers. After having made their digital experience, they make sure it is advertised everywhere it can be advertised.

Domino’s convinced a generation of young people especially that ordering on their app is easy and should be the first thing you do when you want to order food.

This has translated in the UK to a year on year growth in sales from £1billion in 2016 to £1.35billion in 2020. Going from 1013 UK stores in 2016, to 1258 stores across the country in 2020 with an eye towards more expansion and innovation.

Google only overtook Domino’s after the latter had a recent double-dip due to the pandemic. All tech stocks benefitted from the pandemic, as people saw the benefits a technically-equipped society can reap during a global tragedy. Whereas consumer discretionary spending halted worldwide, causing those stocks, like Domino’s, to suffer in their returns.

The fact that Domino’s is rocketing again shows its resilience. In spite of the pandemic, global annual sales increased from $14.3billion in 2019 to $16.1billion in 2020. It punches above its weight class given Google made $160.74billion in 2019 and $181.69billion in 2020.

Domino’s’ strategy for the future is threefold:

Given the wild success both in sales and for investors, Domino’s has been a darling of stock portfolios. As for the future, it’s clear that Domino’s has a great track record of investing in tech. As long as we keep eating pizza, DPZ stock is going to be relevant.

15 July 2026 6 min read

05 July 2026 7 min read

Leave a Reply