Islamic Mortgage Remortgage Guide: What to Do When Your Fixed Term Ends

Ibrahim Khan

02 December 2025 8 min read

Haider Saleem

6 min read

Last updated on:

Islamic mortgages are currently the only genuine solution for Muslims in the UK. It’s a small and relatively new market.

There are 2 main providers of home purchase plan (HPP) products in the UK today though a number of others are technically authorised to issue them. We look at two others after our analysis of the main two banks providing HPPs today.

Here we’ll be looking at:

For a detailed comparison of Islamic mortgage rates, check out our comparison page.

We’ve also written about if Islamic mortgages are cheaper than conventional ones here. In short, no. They are much more expensive.

Al Rayan Bank are the largest and oldest Islamic bank. They have the widest range of Islamic mortgage products in the market, and are well capitalized. That last bit is important – because sometimes banks say they are ready to give out mortgages, but don’t in reality have sufficient money to do that at any great scale.

Al Rayan was the go-to bank when it came to 95/90% LTV Islamic mortgages, but sadly they are now culling that. On average, they are arguably a little bit more relaxed in their underwriting than Gatehouse.

In August 2019, we reported that Al Rayan has a 4/5 average rating based on 216 reviews. Very impressive.

BUT… Writing in November 2020, they’ve dropped to 3.5/5. This is from a significantly larger average rating based on 663 reviews.

With an extra 447 reviews since our last analysis on them, they’ve dipped.

Most people are happy with their services, but there is a sizable majority that aren’t:

People either really like them or really don’t:

There’s been a dip in ‘excellent’ reviews since we last checked in August 2019:

We can’t filter the reviews by products on Trustpilot. Therefore, the 663 reviews could be for any of its products. However, below you can find some relevant ones for mortgages.

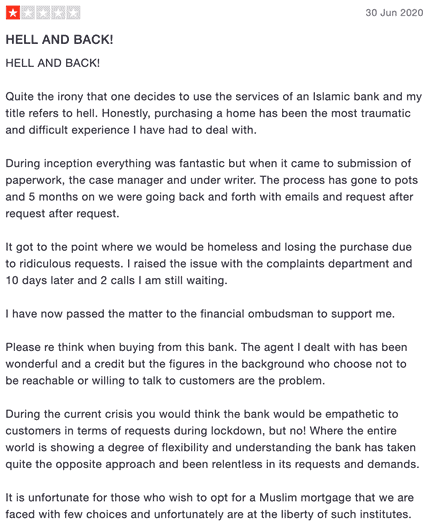

We don’t know the individual circumstances of each review, but we’ll pick the common themes from what we’ve read.

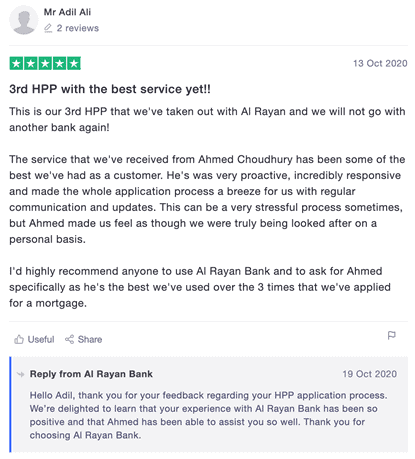

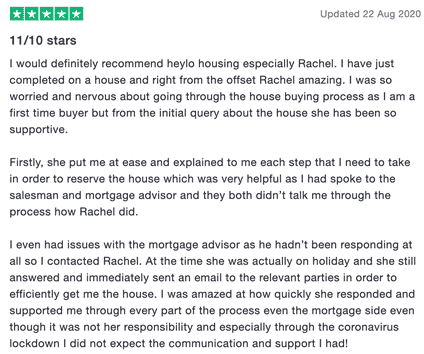

Many of the positive reviews are specifically naming individuals who have been helpful in the process. It’s really nice to see staff going that extra mile and getting recognised for it, like this one here:

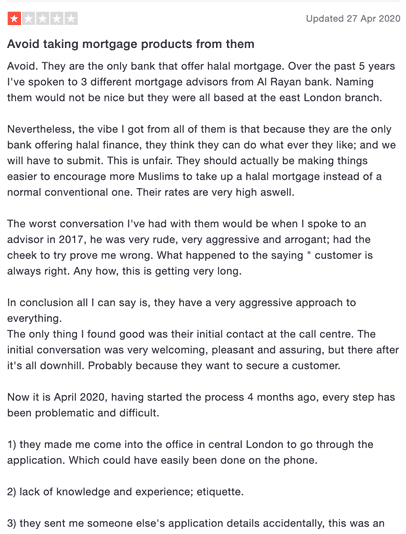

However, we still saw recent complaints about customer service, something we highlighted in our review of Al Rayan in August 2019:

The best thing to do is to use our comparison tool for your circumstances.

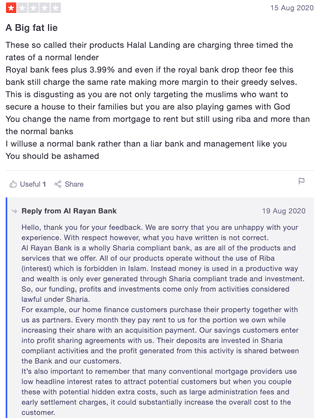

A conventional mortgage will always be cheaper. However, customers have recently complained about the cost of Al Rayan:

In a long reply from the bank, I feel this extract is key to note in the Banks defense…

“Al Rayan Bank does not compete on price with High Street banks. Instead we focus on providing affordable and ethical Sharia compliant banking products which allow our customers to carry out their day-to-day banking requirements without compromising their faith or principles.”

In this article, we’ll compare only to other Islamic mortgage providers.

Let’s compare it to Gatehouse Bank, using a 30-year mortgage term on a £250,000 house, charging a 20% deposit (i.e. borrowing £200,000). Al Rayan are the only Islamic bank offering a 10% deposit mortgage so it would be difficult to compare without changing the example deposit amount.

You should do a comparison for your own particular circumstances (deposit, length of term etc). Don’t forget to factor in that when the rate reverts to the variable rate, you will be exposed to a changing rate (usually pegged in some way to the Bank of England base rate).

Shared ownership – How do AR compare to a relatively well-known shared ownership provider, Heylo Housing?

Check out our detailed review of Al Rayan Bank’s HPP here.

Gatehouse was established in 2007 but has only recently started offering retail HPPs and Buy-to-Lets. It is looking to quickly grow in this market and has aggressively undercut Al Rayan on some of the key HPP products (e.g. the 80% LTV Islamic mortgage).

This competition is only good for the Muslim consumer and we expect customer care standards and pricing to improve as a result.

In August 2019, We conducted our own survey from IFG audience members about their experiences with Gatehouse. The overall results were positive – see them in full here.

Here’s a snippet:

Q: If you were buying a house today, would you use Gatehouse again?

Average answer: 7.5/10

Median answer: 8.5/10

They only have 20 reviews on Trustpilot, not a great sample size. They have averaged at 3.2.

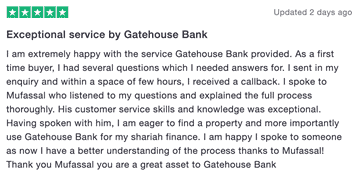

Here’s a good one:

And a not so good one:

In our analysis, mainstream banks come out cheaper by around 25-30% for someone who is buying a house for £250,000 and has a 25% deposit.

Compared to Al Rayan, using the same scenario above (£250k purchase with 25% deposit), their monthly payment comes out at £830.49.

Another point is they don’t make you pay for their lawyers or restrict who you go with. This could save you some money. But the contract does allow for them to charge you for all legal and other expenses they reasonably incur whilst preparing your mortgage documentation.

Ahli is the UK arm of NCB, the second-largest banking group in the Middle East. Their usual clientele are those looking to buy larger, more expensive properties, generally in the London area.

Their products are not suitable for most, but where they do become suitable (for example a 65% LTV mortgage in London where you’re looking to borrow over £250,000), they often have great rates. So for someone who already has an Islamic mortgage and wants to refinance, and lives in London, Ahli might be worth a closer look.

Heylo Housing is an alternative to a mortgage. It provides a shared-ownership model where you can buy back as much (or as little) of your house as you like.

Generally, they are most suitable for those who are otherwise struggling to get an Islamic mortgage with a mainstream Islamic bank – because Heylo’s rates tend to be more expensive and not worth it if you can go for an Islamic bank instead.

The ratings here are incredible – 4.7 stars from 279 reviews.

82% of their reviews are rated as ‘excellent’.

Let’s compare with Al Rayan, sticking with the 20% deposit example above – 20% down on a £250K house.

Here, Heylo would work out slightly cheaper (even factoring in the much higher product fee). We have measured that by looking at the cost over the first 12 months (including product fee) which would be around £11,100 for AR and £10,980 with Heylo (if buying a freehold). But given that you aren’t buying any equity in your house with Heylo, the balance strongly shifts in favor of Al Rayan on pricing alone.

The other factor tipping the balance in favor of Al Rayan here is that Heylo increases their rent every year by 0.75% + RPI (i.e. inflation).

On balance, Al Rayan wins out as the cheaper product here over time.

Like in the comparison with Al Rayan, Heylo comes out cheaper but bear in mind that you’re not buying any equity in your house with that. It also has a higher product fee. In addition, Heylo’s price goes up annually by 0.75% + RPI.

With that in mind, Gatehouse comes out on top overall.

The Islamic banks are almost always the cheaper option long-term, however Heylo Housing and Al Ahli can be a good alternative to consider. Al Ahli if you are buying a high-end property in central London, and Heylo if you are struggling to meet all the requirements of Al Rayan/Gatehouse.

Haider Saleem

Haider is a BBC-trained journalist, trainee solicitor and member of the IFG content team. Haider is a BBC-trained journalist, trainee solicitor and member of the IFG content team.

02 December 2025 8 min read

05 September 2025 11 min read

Leave a Reply