Benefitting 100k+ Muslims every month

Halal wealth made easy

I'm new to investing

No problem at all, we're here to support you through your investment journey

Beginner resources

Start here

Still don't know where to start? Our "start here" breaks it down step by step.

Guides

We have detailed guides in simple English that give you everything you need in bitesize format

I'm an experienced investor

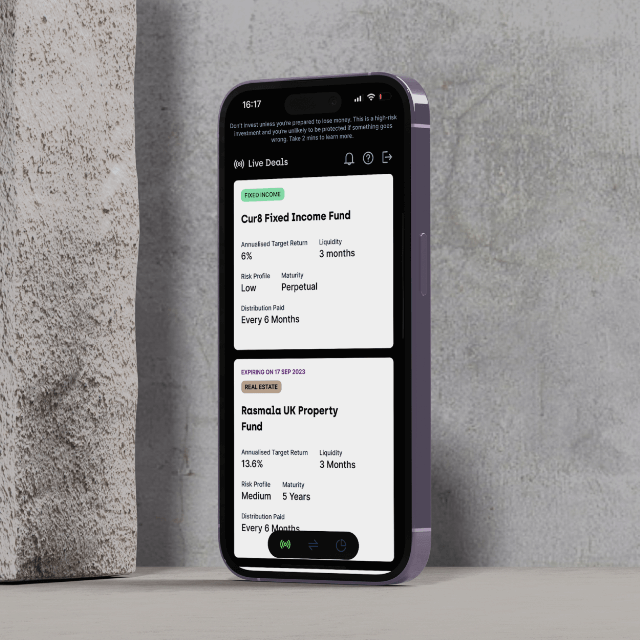

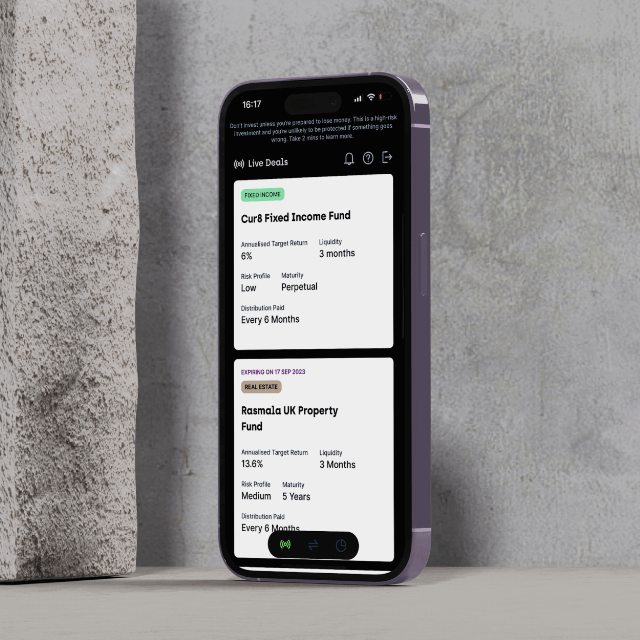

Our investment platform Cur8 Capital provides access to world class funds

Introducing Cur8

Cur8 Capital is IFG's trusted investment platform. Providing you access to our in-house, world class funds in Real Estate, Fixed Income and Private Equity.

As seen on

Why we started IFG

Our Story

IFG was started by Ibrahim and Mohsin back in 2015 as a humble blog alongside our corporate careers.

Our mission is the same it has been from the start. We want to help the Muslim community across the world get back to a level financial playing field.

Read our Story

What the People Say

Latest articles

What IFG will do to help bring about a truly Islamic economy

05 January 2024 8 min read

IFG's Investment Platform

Invest Now