Autumn Budget 2025: What This Means For UK Muslims

Adil Hussain

26 November 2025 6 min read

Ibrahim Khan

Co-founder

3 min read

Last updated on:

Pensions are a boring subject because no one likes to talk about something that will happen in about 40 years’ time. But Muslims in the UK are sleepwalking into losing £13 billion over the next generation.

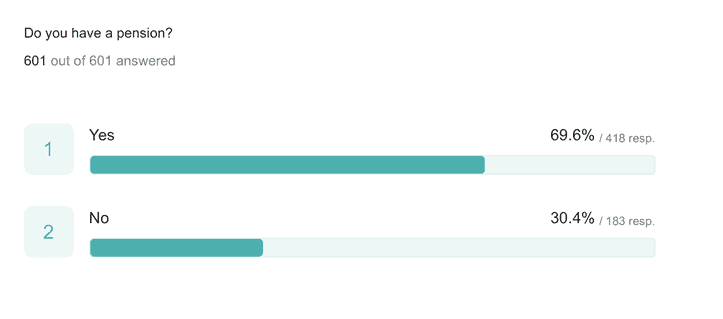

We ran a survey that was answered by 600 of the most financially-savvy Muslims in the UK and the results were alarming.

Let me run you through what we found.

The average UK pension pot after a lifetime of savings is £61,897 [1]. This will buy you around £3,000 in income per year at retirement, which, combined with the maximum state pension, works out around £12,000 per annum. Just about enough to survive on.

But 30.4% of the respondents to our survey said they do not have a pension.

The Muslim population currently stands at around 3.4m in the UK [2] of which 20% are in work [3]. So 680,000 Muslims are in work, and 30% of this group do not have a pension.

30.4% of 680,000 = 206,720.

So 206,720 people do not have a pension.

If they did, they would collectively hold £12.8 billion. As it stands they have nothing.

This is actually a pretty big deal for not just Muslims – but the entire UK. Because this £12.8 billion shortfall will be made up from the state pension and benefits.

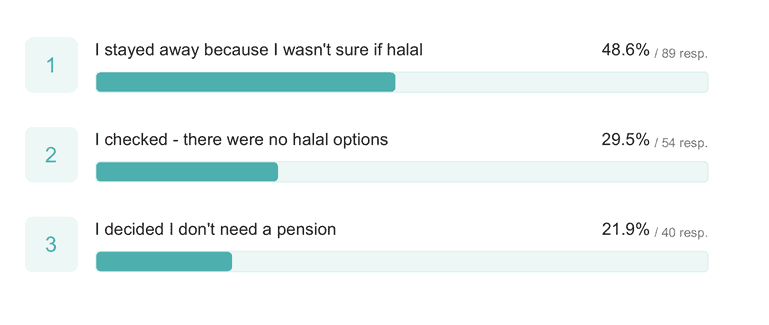

When we asked those who do not have a pension, why they don’t have a pension, their responses are below:

78.1% of the people who do not have a pension do not have it explicitly because of sharia-compliance concerns.

Either this is because they checked and found no halal options or because they didn’t have the relevant information or awareness to be able to make their mind up if a pension is sharia-compliant and stayed away because of that.

In other words, the two major things that need to happen to stop Muslims losing £13 billion over a generation is the following:

To address (2) we have written a really really simple guide here to work out if your pension is halal or not. Much more needs to be done.

But to address (1) we need a concerted effort from the Muslim community, government, employers, and pension providers.

If the previous points were not bad enough, it gets worse.

Of the 69.6% who did have a pension, 39.5% reported that their employer does not have an Islamic pension option. So in total, ~40% of the Muslims who do have a pension are sadly in pensions that go against their beliefs as there is no alternative.

This also coheres with government-commissioned Ipsos Mori findings in a study they did in 2011 [4] that Muslims, if given the option, would go for sharia-compliant funds.

The survey respondents were from our subscriber list. In other words, the survey respondents were the most digitally-savvy, financially literate, engaged and interested people in the Muslim community. They are also much more likely to be employed. In reality, these numbers are likely to be worse than our findings as many of the Muslim community are not digitally-savvy and financially literate, and some are not in employment either.

The other important point to note here is that dozens of large employers – including public companies – do not have an Islamic pension option as part of their workplace pension. We’ll be working hard to get these employers to change their minds and pension practices.

There is a tremendous amount to be done by us all.

The one simple thing you can all do to help is just raise awareness. Share this article with those in your networks. Particularly those who you know may not have a pension. Every little helps.

The other thing you can do – if you haven’t already – is take the survey and give us your answers in 30 seconds. The closer we can get to 1000 responses, the more credible the results are and the more likely change becomes.

Ibrahim Khan

Co-founder

Ibrahim is a published author and Islamic finance and investment specialist. He is currently the CEO of Islamicfinanceguru and its sister investment company Cur8 Capital. He holds a BA in Philosophy, Politics, and Economics from the University of Oxford, an Alimiyyah degree from the Al Salam Institute, and an MA in Islamic Finance. Prior to setting up Islamic Finance Guru, Ibrahim was a corporate lawyer. He trained at Ashurst LLP and then specialised in private equity and venture capital funds at Debevoise & Plimpton LLP. He holds a Diploma in Investment Advice & Financial Planning & Certificate in Investment Management. Publication: Halal Investing for Beginners: How to Start, Grow and Scale Your Halal Investment Portfolio (Wiley) Ibrahim is a published author and Islamic finance and investment specialist. He is currently the CEO of Islamicfinanceguru and its sister investment company Cur8 Capital. He holds a BA in Philosophy, Politics, and Economics from the University of Oxford, an…

26 November 2025 6 min read

23 September 2025 4 min read

02 July 2025 6 min read

Leave a Reply