Calculating Zakat on Shares – Paying Zakat in Islam | IFG

In this Article

Mohsin Patel

Co-founder

5 min read

Last updated on:

Ramadan tends to be zakat season, and we’ve been receiving queries on how exactly to calculate the zakat owed on shares. We have discussed this before in this article, but this present article is designed to be a one-stop guide. By the end, you should be clear on how much zakat to pay on your shares.

But before we dive in, you should also definitely download our definitive guide (also footnoting multiple fiqhi positions) on zakat on a range of common investments here. You should also definitely check out our zakat calculator here.

If you’d rather watch our zakat guidance, check it out here:

How hard can it be?

There are broadly 3 main ways in which you can work out how much zakat to pay on your shares.

1. The market value approach;

2. The zakatable assets approach; and

3. The 25% approach.

We’ll go into each route under a separate heading, but there’s an important question to be answered first.

Which of the 3 approaches is suitable for my shares?

The answer to that is that it depends on what your approach to investing in shares is. If you are buying shares with a short-term trade in mine and looking to profit in the short term, then the market value approach is most suitable.

If, however, you buy shares with a view to holding them – and perhaps selling them at some indeterminate point in the future if you’ve turned a nice profit – then the zakatable assets approach or the 25% approach is for you.

You might wish to consult a knowledgeable scholar about which approach to take depending on your circumstances.

The Market Value Approach

This is really quite straightforward. Simply treat the value of your share portfolio in the same way as you would treat cash, and pay 2.5% of the entire portfolio value as zakat.

Remember though, it’s what your shares are worth in the market at the time of paying zakat, not what you bought them for. For instance, if you invested £20,000 in shares and those shares are now worth £25,000, you would pay 2.5% of £25,000, which is £625.

The Zakatable Assets Approach

If you have a longer-term view in mind for your shares, it is accepted that instead of taking the value of your shares as the basis for zakat, what you can do is look into the heart of the company and pay zakat on the zakatable assets of that company.

Generally speaking, the zakatable assets of a company are those things which are liquid – things like cash, stock, etc. You do not pay zakat on illiquid things like property and machinery in a company.

You can look at the liquid assets of a company by looking in their latest accounts. Each company’s account will differ very slightly but will be broadly similar and you can make the analysis in a fairly straightforward manner as all you are looking for are liquid assets.

Let’s look at an example using well-known FTSE100 company AstraZeneca. I haven’t assessed whether or not they are sharia-compliant (see this article on how to do that), but I am using them just as an illustration on how to work out zakatable assets.

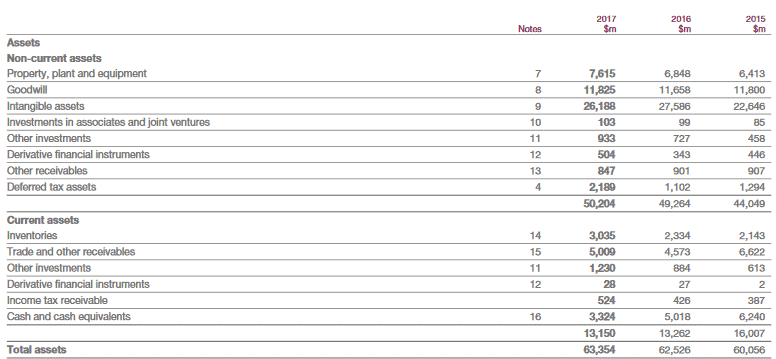

You will need to navigate to the assets section of the balance sheet in the accounts. For AstraZeneca, that looks like this:

Looking at the non-current assets, it is clear that none of these are liquid so we can disregard all of these immediately.

Turning to the current assets, we see certain items. These items are reproduced here along with my view on whether these are liquid – and therefore zakatable – or not:

- Inventories – liquid;

- Trade and other receivables – liquid;

- Other investments – liquid (having read note 11);

- Derivative financial instruments – liquid;

- Income tax receivable – liquid;

- Cash and cash equivalents – liquid.

Thus on my analysis, all of the current assets of AstraZeneca are liquid. If you are unsure about whether an asset is liquid or not, read the note to it, and if you are still unsure, either ask somebody qualified or add it in just to be sure.

So we add all those zakatable assets up and it tells us that $13.15bn (£9.88bn) of assets in AstraZeneca are zakatable.

Having worked out what portion of the company is zakatable, we need to work that out as a percentage of the entire company. We do that by taking the current market valuation of AstraZeneca and working out the percentage.

At the time of writing, AstraZeneca’s market capitalisation (its market value, taken as total number of shares in issue multiplied by share price) is £69.4bn (source link). Thus, zakatable assets comprise 19% of the company.

Now let’s say your shares in AstraZeneca are worth £10,000 at the time of calculating your zakat. Again, remember it’s what your shares are worth in the market, not what you bought them for. On £10,000, you 19% of it (i.e. £1,900 is zakatable). You then work out 2.5% of £1900, to give you your final zakat amount on your AstraZeneca shares, which would be £47.50.

Repeat this across your entire share portfolio.

The 25% Approach

This is similar to the above, except that if you do not want to work out the actual number of zakatable assets within a company, you can take a safe approach of saying 25% of the company’s assets are zakatable.

So in the above example of your AstraZeneca shares being worth £10,000, you simply say 25% (i.e. £2,500) of that is zakatable, then work out 2.5%, which would give £62.50.

This is an approach that is endorsed by a number of scholars and charities – including National Zakat Foundation who undertook a detailed analysis of various funds and determined that the 25% was a good proxy percentage to use.

Conclusion

So there we have it – the 3 approaches to calculating zakat on your shares!

You can very simply calculate your zakat using our calculator here.

Mohsin Patel

Co-founder

Mohsin is the co-founder of IslamicFinanceGuru, an Oxford graduate and a Forbes 30 under 30 alumnus. He's a former corporate lawyer at one of the world's largest US firms. Whilst running IFG, Mohsin is also actively interested and invested in the web3/crypto space. Publication: Halal Investing for Beginners: How to Start, Grow and Scale Your Halal Investment Portfolio (Wiley) Mohsin is the co-founder of IslamicFinanceGuru, an Oxford graduate and a Forbes 30 under 30 alumnus. He's a former corporate lawyer at one of the world's largest US firms. Whilst running IFG, Mohsin is also actively interested and invested in…

Leave a Reply